Data Intelligence Meets Regulatory Innovation: Barry James Joins GECA

The Man Who Built the Evidence Base for Crowdfunding - and Changed Regulation to Match Reality

In 2012-13, while most policymakers still viewed crowdfunding as an experimental curiosity, Barry James was doing something radical: tracking every campaign, building the data infrastructure to prove crowdfunding worked, and simultaneously architecting the regulatory change needed to let it flourish.

A decade later, that dual approach - rigorous data intelligence combined with regulatory innovation - has transformed how governments worldwide approach fintech regulation.

Now, GECA welcomes Barry as Strategic Advisor, that same systems-level thinking comes to the challenge of building borderless crowdfunding.

When Data Meets Disruption

Barry didn't just write about crowdfunding's potential. He created The Crowd Data Center, tracking over 900,000 campaigns across more than a decade - the world's largest crowdfunding dataset. This wasn't academic curiosity. It was infrastructure.

"We needed evidence, not anecdotes," explains Barry, "Regulators don't move on enthusiasm. They move on data that demonstrates market function, investor behaviour, and risk profiles. The Crowd Data Center became the analytical foundation that helped legitimize crowdfunding as a mainstream funding channel - first in the UK, then globally."

That data revealed patterns nobody else could see. His "State of the Crowdfunding Nation" reports, published quarterly since 2014, didn't just track volume. They exposed the emergence of what Barry termed the "eFunding Escalator" - a new capital formation pathway where crowdfunding served as validation for traditional finance to follow.

Yet more groundbreaking was "Women Unbound," research conducted with PwC analyzing 450,000+ campaigns. The findings challenged conventional wisdom: women-led crowdfunding campaigns reached their targets more often than men-led campaigns - a stark contrast to the expectations there have been in traditional entrepreneurship where women receive barely two percent of venture funding.

"The data told us something profound about access and bias," Barry notes. "Crowdfunding wasn't just democratizing capital access. It was revealing how traditional gatekeepers had systematically failed entire demographics. That evidence became impossible for policymakers to ignore."

The Regulatory Architect

But data alone doesn't change systems. In August 2012, Barry published a proposal in Real Business that would reshape UK financial regulation: the Financial Conduct Authority (then FSA) should create an "Innovation Unit" specifically designed to enable fintech innovation while maintaining investor protection.

The idea was revolutionary. Financial regulators traditionally approached innovation with caution, if not outright resistance - 'Prevention Mindset'. Barry's proposal flipped the model: regulation should also support innovation, without compromising protections.

Barry explained at the time. "We had regulatory frameworks designed for 20th-century financial institutions being applied to 21st-century technology platforms. The mismatch was strangling innovation that could benefit millions of underserved businesses and investors."

He didn't just propose the concept. He campaigned for it. Through the Westminster Crowdfunding Forum he co-founded and the All-Party Parliamentary Group on Crowdfunding and Non-Bank Finance, Barry worked directly with legislators to make the case.

In 2014, the FCA Innovation Unit ("Hub") launched, beginning the transforming the UK's regulatory culture. The impact rippled globally. Today, more than 95 regulators have replicated the model, specifically designed to enable fintech while protecting ecosystem participants. The innovation has since spread across 18 fields from aerospace and AI to nuclear.

"Barry's work on the FCA Innovation Unit represents exactly the kind of systems thinking we need for global crowdfunding harmonization," said Andy Field, GECA Steering Committee Executive Lead. "He didn't just advocate for less regulation or more innovation. He architected a framework that enabled innovation, serving rather than endangering protections - and proved it could work at national scale. Creating a model that is now referenced worldwide."

From Westminster to Global Standards

Barry's influence extends beyond single initiatives. As Co-Chair of the Westminster Forum on Crowdfunding and Non-Bank Finance, he co-created the institutional space where regulators, platforms, entrepreneurs, and policymakers could engage in evidence-based dialogue.

These weren't talking shops. They were working sessions that shaped policy at the highest levels. When the UK government needed to understand crowdfunding's role in SME finance, they looked to Barry's data. When the European Commission sought insights on alternative finance regulation, Barry's research informed their approach.

His book, "New Routes to Funding - The Handbook of Modern Funding," became required reading for business advisors and entrepreneurs navigating the new funding landscape. Industry leaders called it a "page turner" and "gamechanger" - unusual praise for a book about capital formation mechanics.

"Barry has this extraordinary ability to grasp complicated systems and translate them for ordinary people with metaphors that border on the lyrical," noted Dr. Julie Gregory, a long-time collaborator. "Always visionary, always reaching for the future."

Beyond Crowdfunding: Blockchain, AI, and Digital Money

Barry's expertise doesn't stop at crowdfunding. As Founding Chair of the British Blockchain and Frontier Technologies Association, and a founding columnist for City AM's CryptoInsider, and The Fintech Times, he's tracked the evolution of blockchain, tokenization, and central bank digital currencies (CBDCs) with the same data-driven rigour he brought to crowdfunding.

His Remaking Money project explores how CBDCs will transform national currencies - changes he describes as potentially as significant as the internet itself. His Humane Economics work challenges the financialized thinking that he argues damages both society and planetary ecology. He has said:

"Eighty-six percent of central banks globally are now working on digital currencies," Barry observed. "This will touch everyone. At every stage there will be opportunities and pitfalls. We need the same kind of evidence-based, systems-level thinking we applied to crowdfunding regulation - but at an even larger scale."

This polymathic approach - spanning crowdfunding data, regulatory architecture, blockchain technology, AI implications, and monetary systems - represents exactly the cross-disciplinary thinking required for global coordination.

"What we need in global crowdfunding harmonization isn't expertise in just one domain," Field emphasized. "We need people who understand how technology, regulation, data, and institutional behavior interact across complex systems. Barry's four decades navigating those intersections - in the NHS with health tech, in financial services with fintech, in policy with regulatory innovation - gives him unique translation capability between worlds that typically don't speak the same language."

The GECA Mission

Barry's appointment comes as GECA advances from dialogue to infrastructure-building. The organization's mission - creating transparent, credible, borderless equity crowdfunding markets - requires exactly the combination Barry brings: data intelligence that builds the evidence base, regulatory expertise that enables practical frameworks, and systems thinking that connects fragmented pieces into coherent wholes.

"I'm excited to join GECA at this pivotal moment," Barry said. "We're at an inflection point with huge challenges and even greater potential. Equity crowdfunding could remain trapped in fragmented national silos - or could fulfil its potential as global infrastructure. If we have the drive and ambition to build the standards, data interoperability, and trust architecture to make this a reality."

GECA's first priorities include advancing work on disclosure standards, platform interoperability, and evidence-based advocacy with regulators. The Crowd Data Center's decade-plus dataset provides GECA with unmatched analytical depth on campaign performance, investor behaviour, and market dynamics across jurisdictions - insights that inform both standards development and regulatory dialogue.

"Barry doesn't just bring data or regulatory expertise in isolation," Field noted. "He brings the methodology for using data to drive regulatory evolution - the same approach that created the FCA Innovation Unit. That's transformative for GECA. We're not just advocating for better rules. We're building the evidence base that helps regulators worldwide understand what works."

Looking Ahead

Barry's career trajectory reveals a consistent pattern: identify emerging technology or market structure, build the data infrastructure to understand it rigorously, create the institutional spaces for stakeholder dialogue, and architect the frameworks that enable innovation while protecting participants.

He did it in the NHS during the 1990s, pioneering electronic health information transfer with what became nationally known as the "Sheffield Project." He did it in fintech with the FCA Innovation Unit. He did it in crowdfunding with The Crowd Data Center and Westminster Forums.

Now he's applying that same methodology to GECA's mission of borderless crowdfunding markets.

"The technology for cross-border crowdfunding exists," Field observed. "The demand exists - investors already invest internationally, and platforms already scale across borders. What's missing is the coordinated infrastructure: common disclosure standards, interoperable data schemas, regulatory frameworks that recognize each other's gatekeeping. That's not a technology problem. It's a coordination problem. And coordination problems require the kind of multi-stakeholder, evidence-based, systems-level work that GECA champions."

With Barry's appointment, GECA gains not just UK representation but four decades of proven infrastructure-building expertise - the data intelligence, regulatory architecture capability, and institutional relationships needed to turn fragmentation into coordination.

"We're building the rails for global crowdfunding," Field concluded. "Barry's been building rails his entire career - in health tech, in fintech, in regulatory innovation. He knows what it takes to turn aspiration into infrastructure. Welcome to the team, Barry. Let's build what comes next."

About Barry James

Barry James is a polymathic analyst, strategist, and transition architect with over 40 years of pioneering expertise in technology, finance, and social innovation, with impact across ~100 nations. As Founder and CEO of The Crowd Data Center, he created one of the world's leading crowdfunding data resources, tracking 900,000+ campaigns over more than a decade.

Barry conceived and successfully advocated for the creation of the UK Financial Conduct Authority's Innovation Unit (2012-2014), transforming regulatory culture to enable fintech innovation - a model since replicated in approximately 100 jurisdictions globally. As author of "New Routes to Funding - The Handbook of Modern Funding" and founding Co-Chair of the Westminster Forum on Crowdfunding and Non-Bank Finance, he has shaped policy dialogue at the highest levels.

His "State of the Crowdfunding Nation" reports and groundbreaking "Women Unbound" research with PwC provide evidence-based insights demonstrating how crowdfunding unlocks entrepreneurial potential. With deep expertise spanning equity crowdfunding, blockchain, AI, and central bank digital currencies, Barry brings systems thinking and institutional relationships essential to GECA's mission of harmonized global crowdfunding standards.

About GECA

The Global Equity Crowdfunding Alliance (GECA) is a neutral, industry-led network bringing together equity crowdfunding platforms, national associations, regulators, policymakers, and technology providers to build transparent, credible, borderless equity crowdfunding markets.

GECA's mission is to foster dialogue, alignment, and practical pathways for cross-border collaboration - addressing regulatory fragmentation, advancing interoperable infrastructure, and creating the standards and trust architecture that enable equity crowdfunding to fulfill its global potential.

Learn more: https://thegeca.org

Join GECA: https://thegeca.org/join

Media Contact:

Andy Field

GECA Steering Committee Executive Lead

info@thegeca.org

GECA Appoints Jill Storey: Big 4 Partner Turned Crowdfunding Pioneer

GECA Strengthens Asia-Pacific Leadership with Appointment of Renowned Finance and Crowdfunding Expert

Former Big 4 Partner, Early UK Crowdfunding Pioneer, and Ocean Climate Finance Leader Brings Institutional Rigor and Entrepreneurial Insight to Global Harmonization Mission

The Global Equity Crowdfunding Alliance (GECA) today announced the appointment of Jill Storey as Strategic Advisor for Australia to its Steering Committee, marking a significant expansion of the organization's Asia-Pacific expertise and regulatory insight.

Jill brings over 25 years of global financial expertise spanning four continents, pioneering crowdfunding experience from the sector's earliest days, and proven impact investing leadership at the intersection of finance, innovation, and climate solutions.

From Big 4 Partnership to Crowdfunding Pioneer

Jill's career foundation was built through partnerships at three of the world's most prestigious professional services firms - Andersen, KPMG, and Deloitte - across the UK, Europe, Hong Kong, and Australia. In these roles, she advised global financial institutions and multinationals in energy and resources sectors on complex cross-border tax strategy, risk management, and governance issues for global workforces.

"The expertise required to navigate multi-jurisdictional regulatory frameworks, manage cross-border compliance, and advise institutions on strategic risk is exactly what GECA needs as we work toward harmonized global crowdfunding standards," said Andy Field, GECA Steering Committee Executive Lead. "Jill doesn't just understand regulatory complexity theoretically - she's lived it at the highest institutional level across four continents and multiple regulatory regimes."

But what sets Jill apart is her rare combination of institutional rigor and entrepreneurial agility. In 2012, following the London Olympics, she recognized crowdfunding's potential to democratize access to finance and founded a donation-based crowdfunding platform in the UK called Inspire a Star, designed to help children and young people realize their sporting dreams.

This wasn't a side project - it was a fundamental shift from advising institutions to building infrastructure that served underrepresented communities directly.

Building Australia's Equity Crowdfunding Framework

After relocating to Australia, Jill acquired and developed ReadyFundGo, an Australian reward-based crowdfunding platform focused on social entrepreneurs, innovators, and startups. Her hands-on platform experience provided invaluable insight into what makes crowdfunding work in practice - not just in regulatory theory.

Building on this experience, Jill worked closely with several Australian crowdfunding platforms during a critical period: the early implementation of Australia's regulated equity crowdfunding framework. She supported two Australian platforms in obtaining their ASIC crowd-sourced equity funding licenses - navigating one of the world's most progressive regulatory environments for retail equity investment.

Her work across donation, reward, and equity-based crowdfunding models provides a comprehensive perspective on alternative finance evolution that few practitioners can match.

Governance, Policy Leadership, and Industry Development

Since 2017, Jill has served as Non-Executive Board Member of the Crowdfunding Institute of Australia, contributing to industry development and dialogue around crowdfunding and emerging forms of digital finance. Her governance experience spans corporate organizations, not-for-profits, and early-stage ventures - bringing practical insight into building sustainable, well-governed crowdfunding platforms and markets.

"GECA isn't just about platforms - it's about building trustworthy, well-governed ecosystems that regulators, investors, and issuers can rely on," Field emphasized. "Jill's board-level governance experience across multiple organizational types gives her the systems-level perspective we need to help platforms professionalize while maintaining the entrepreneurial spirit that makes crowdfunding powerful."

Impact Investing and Climate Finance Leadership

Currently serving as Ocean CO2 Removal Advisor to the World Ocean Council, Jill exemplifies the intersection of finance, innovation, and impact investing. She works across the global marine carbon dioxide removal (CDR) ecosystem on commercialization, policy alignment, and measurement, reporting, and verification (MRV) integrity - advancing high-integrity, ocean-based carbon removal solutions while maintaining rigorous standards for commercialization and governance.

Her focus on ocean-based climate solutions addresses one of the most critical challenges facing global climate strategy. As equity crowdfunding increasingly channels capital toward sustainable innovation, climate tech, and impact ventures, Jill's expertise in structuring high-integrity impact markets becomes directly relevant.

Jill's credentials reflect her commitment to combining theoretical rigor with practical application. She holds an MBA, a Master's in Environmental Science, and is both a Chartered Accountant and Chartered Taxation Specialist.

Why This Appointment Matters for GECA

Jill's unique combination positions her perfectly to advance GECA's mission of creating transparent, credible, borderless equity crowdfunding markets. Her institutional finance expertise - twenty-five years advising global institutions across four continents - provides deep understanding of how institutions evaluate regulatory complexity. Her hands-on experience supporting platforms through ASIC licensing offers practical insight into operationalizing progressive regulation. Her multi-model crowdfunding experience and climate finance leadership demonstrate ability to structure high-integrity markets that balance innovation with credibility.

"I'm honored to join GECA's Steering Committee at such a pivotal moment for global crowdfunding," Jill said. "Throughout my career - from advising multinational institutions on cross-border governance to founding platforms that help entrepreneurs bring their ideas to life - I've seen firsthand how fragmentation creates friction and how coordination unlocks potential. Equity crowdfunding has proven it can democratize access to capital, support underrepresented founders, and channel investment toward innovation that matters. But for it to reach its full potential globally, we need the kind of regulatory clarity, platform interoperability, and trust infrastructure that GECA is building."

Australia's equity crowdfunding framework, regulated by ASIC, represents one of the more progressive approaches globally. The crowd-sourced equity funding (CSEF) regime allows eligible companies to raise up to AUD 5 million per year from retail and wholesale investors through licensed intermediaries. Jill's direct experience helping platforms navigate ASIC licensing during this framework's early implementation provides GECA with valuable insights into what works when translating regulatory intent into operational reality.

"Jill's appointment represents exactly the kind of expertise GECA needs as we move from dialogue to infrastructure-building," Field noted. "She brings the rare combination of Big 4 institutional rigor and hands-on crowdfunding platform experience. Her work supporting Australian platforms through ASIC equity crowdfunding licensing is particularly valuable -Australia's framework is one of the most progressive globally, and Jill's direct experience gives her insight into what works, what doesn't, and how to translate regulatory intent into platform practice."

Looking Ahead

Jill's appointment comes at a pivotal time for GECA and the global equity crowdfunding ecosystem. As regulatory frameworks mature, technology enablers like tokenization and AI emerge, and cross-border activity increases, the need for coordinated standards, interoperable infrastructure, and trust architecture becomes more urgent.

GECA's work focuses on creating practical pathways for cross-border collaboration by addressing regulatory fragmentation, advancing interoperable platforms and data standards, and building the evidence base that helps regulators, platforms, and policymakers make informed decisions.

Jill's appointment strengthens GECA's ability to deliver on this mission by bringing direct regulatory licensing experience, multi-stakeholder governance expertise, impact investing rigor, entrepreneurial insight, and climate finance leadership that connects crowdfunding to broader sustainable finance trends.

Australia's representation on GECA's Steering Committee strengthens the organization's Asia-Pacific presence at a critical time, enabling cross-jurisdictional learning from one of the world's most advanced equity crowdfunding regulatory frameworks.

About Jill Storey

Jill Storey is a finance and crowdfunding expert with over 25 years of global experience spanning institutional finance, entrepreneurship, governance, and impact investing. A former Partner with Andersen, KPMG, and Deloitte across the UK, Europe, Hong Kong, and Australia, she advised global financial institutions and multinationals on complex cross-border strategy, risk management, and governance.

An early crowdfunding pioneer, Jill founded a donation-based platform in the UK in 2012 and later owned and developed an Australian reward-based platform. She has worked closely with crowdfunding platforms across donation, reward, and equity models, including supporting two Australian platforms in obtaining ASIC crowd-sourced equity funding licenses.

Since 2017, Jill has served as Non-Executive Board Member of the Crowdfunding Institute of Australia. Currently Ocean CO2 Removal Advisor to the World Ocean Council, she advances high-integrity ocean-based carbon removal and climate markets. Jill holds an MBA, Master's in Environmental Science, and is a Chartered Accountant and Chartered Taxation Specialist.

About GECA

The Global Equity Crowdfunding Alliance (GECA) is a neutral, industry-led network bringing together equity crowdfunding platforms, national associations, regulators, policymakers, and technology providers to build transparent, credible, borderless equity crowdfunding markets.

GECA's mission is to foster dialogue, alignment, and practical pathways for cross-border collaboration - addressing regulatory fragmentation, advancing interoperable infrastructure, and creating the standards and trust architecture that enable equity crowdfunding to fulfill its global potential.

Learn more: https://thegeca.org

Join GECA: https://thegeca.org/join

The Crowd Goes Global: Inside the Push to Fix Equity Crowdfunding's Fragmentation Problem

Equity crowdfunding is already crossing borders. The rules aren't keeping up - and a new alliance of industry veterans thinks that has to change.

From 49 countries on Zoom to one shared problem

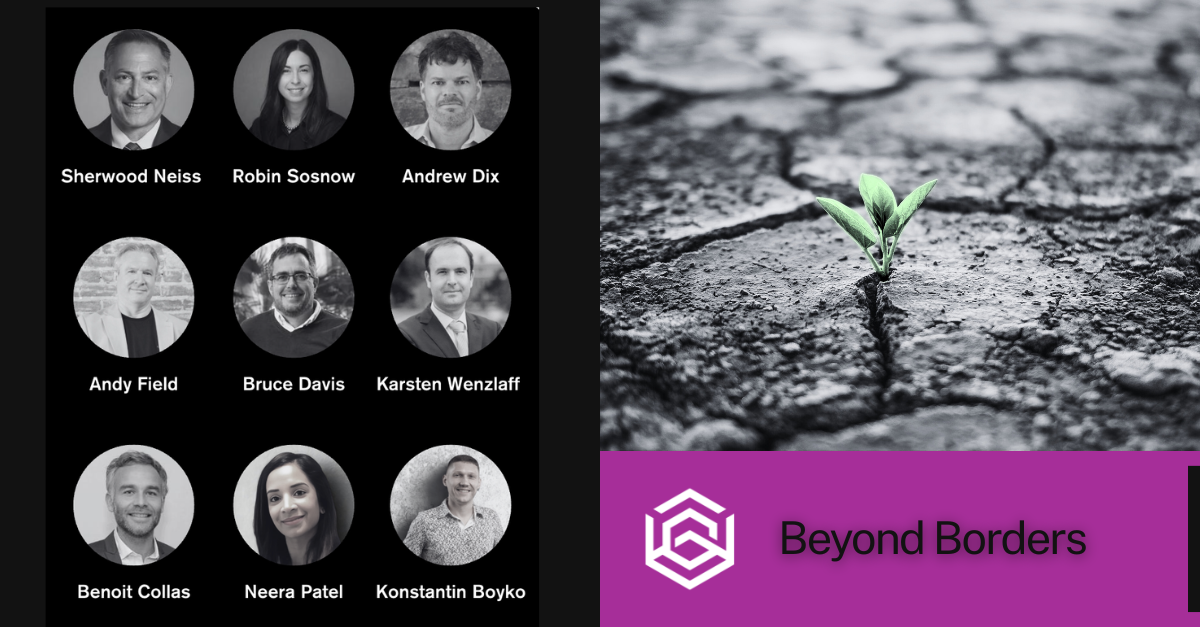

When the Global Equity Crowdfunding Alliance (GECA) convened a joint webinar with Crowdfund Insider and the European Digital Finance Association (EDFA), 49 countries dialed in to talk about a single, stubborn challenge: how to turn today’s patchwork of national rules into a genuinely connected global ecosystem for crowdfunding.

As GECA steering committee lead Andy Field put it, crowdfunding is already global in practice - investors and platforms are operating across borders every day - but still fragmented in regulation, infrastructure and coordination.

The consequences are concrete:

- Founders who want to raise across borders face multiple regulatory systems, overlapping compliance regimes and incompatible technology standards.

- Investors struggle to access deals outside their home market.

- Platforms duplicate costs, and offers that should be global remain stubbornly local - just when capital is urgently needed for SMEs, climate projects, infrastructure and innovation.

GECA’s answer is deliberately modest and ambitious at the same time: not a lobbying machine for one preferred regime, but a neutral, industry‑led network that brings together platforms, investors, founders, industry associations, regulators, policymakers and tech providers to create practical pathways for cross‑border collaboration.

This webinar -anchored by moderator Andrew Dix of Crowdfund Insider with contributions from US securities lawyer Robin Sosnow, German policy veteran Karsten Wenzlaff, UK pioneer Bruce Davis, and a second‑half line‑up featuring Konstantin Boyko, Neera Patel, Sherwood “Woodie” Neiss and Benoit Collas - was a high‑level tour of where those pathways might emerge.

The US: Jobs Act 2.0 and a market “almost there”

To understand where online capital formation is going, the panelists began by looking back. In the United States, Robin Sosnow traced the evolution from the 2012 JOBS Act to today’s mix of exemptions that underpin investment crowdfunding.

Regulation D was first to change, allowing general solicitation in 2013 and effectively legitimizing online private placements to accredited investors. Regulation A followed in 2015, re‑emerging as “Reg A+” with the ability to raise from retail investors under a two‑tier system that now allows up to 75 million dollars under Tier 2 - a structure increasingly attractive to later‑stage private companies eyeing alternatives to a traditional IPO.

Then came Regulation Crowdfunding (Reg CF) in 2016, which legalized retail investment crowdfunding but initially capped offerings at 1 million dollars per 12‑month period. The cost of legal, portal and accounting work made that cap hard to justify, and early adoption was modest.

The real inflection point arrived with 2021 rule changes:

- The Reg CF limit rose to 5 million dollars.

- “Testing the waters” became permissible.

- Crowdfunding vehicles (SPVs) were allowed, solving the “messy cap table” concern by pooling investors into a single LLC on the issuer’s cap table.

Since then, the various JOBS Act exemptions have started to function as a coherent capital stack for private companies, rather than disconnected experiments.

The SEC continues to refine the rules at a more granular level. Recent compliance and disclosure interpretations clarified, for example, that Reg CF investor limits for retail investors are calculated on a calendar‑year basis, even though issuer offering caps are measured on a rolling 12‑month period. On the Reg A side, the Commission has confirmed that issuers can file draft offering statements confidentially, shielding their initial disclosures and SEC comment correspondence from competitors until they choose to go public.

Legislatively, the Invest Act currently before the US Senate would raise the threshold at which very small Reg CF issuers must provide reviewed financial statements - moving it from around 100,000 dollars to 250,000 dollars, with scope to increase that to 400,000 dollars over time. That change, Robin argued, will matter for true micro‑offers, even if a deeper fix would also relax the requirement for GAAP‑based financials at the very bottom of the market.

The more controversial frontier is the accredited investor definition. The policy conversation is shifting from purely wealth‑based criteria toward some form of knowledge‑based certification - potentially unlocking a broader pool of sophisticated investors without lowering standards.

Through all of this, Dix framed a simple success condition: three stakeholders must win, or the system fails. Platforms must be profitable; issuers must raise the capital they need; investors must see a reasonable path to returns. Technology, he argued, is finally bringing that goal into view - if regulation can keep up.

Europe: ECSPR’s promise - and a 5 vs 12 million problem

On the other side of the Atlantic, Europe has spent the past decade wrestling with its own fragmentation. When early drafts of the European Crowdfunding Service Providers Regulation (ECSPR) were written ten years ago, some EU member states did not even permit online securities offerings. Others had bespoke frameworks, but cross‑border operations remained painfully complex.

ECSPR was designed to change that by harmonizing how platforms are licensed, what they may offer, and how they must report. Under the framework:

- Platforms can intermediate transferable securities (mainly shares) and loans.

- Issuers can raise up to 5 million euros per year across all platforms, EU‑wide.

- Instead of hard investor caps, platforms must segment investors as “sophisticated” or “non‑sophisticated” and apply knowledge and appropriateness tests for the latter - an approach borrowed in spirit from the UK.

- Issuers must provide a six‑page Key Investment Information Sheet (KIIS), the EU’s surprisingly user‑friendly “KIIS” document, which serves as a standardized disclosure across member states.

In theory, ECSPR created a unified passport for platforms and issuers. In practice, Karsten Wenzlaff noted, fragmentation lingers in subtler ways:

- National regulators interpret and apply the rules differently.

- Investors still display a strong “home bias” -Spanish investors prefer Spanish platforms and SMEs, even though they could easily back Slovak or German deals.

The most striking anomaly is the fundraising cap. Under separate prospectus rules, a company can raise up to 12 million euros from the public on its own site without a full prospectus, as long as it stays within the EU Listing Act thresholds and structures the offer correctly. The moment it uses a regulated crowdfunding platform, however, it is constrained to 5 million euros in aggregate across all platforms.

That inversion - platforms being more constrained than direct offerings - cuts against the original policy intent of using regulated platforms to channel capital to SMEs and scale‑ups. It also feels increasingly out of step with the capital requirements of modern sectors, from AI to deep tech.

An ECSPR working group led by platforms and associations has already published an 80‑page evaluation report, and the European Commission is formally required under Article 45 of ECSPR to review the regime this year. Wenzlaff and his peers are pushing to align the crowdfunding cap with the 12‑million‑euro threshold used elsewhere in EU capital markets legislation, with an expectation that inflation and market development may eventually push that number higher.

Secondary markets are another fault line. Today, ECSPR platforms can host bulletin boards, but cannot operate true order‑matching marketplaces. That leaves issuers and investors with limited liquidity and constrains the ability of crowdfunding to feed into a broader private‑markets stack.

Tokenization could, in theory, help. Wenzlaff sees three immediate use cases:

- Dynamically splitting and routing fees when multiple platforms syndicate a deal, recognizing the additional work done by the “originating” platform.

- Enabling compliance checks and investment limits to be enforced on‑chain, without platforms having to share raw investor data with competitors.

- Providing a decentralized, tamper‑resistant channel for post‑investment reporting, ensuring that all investors receive the same information at the same time, regardless of which platform they used.

But as Benoit Collas of impact‑focused EU platform Enerfip emphasized, none of this is painless. Even within ECSPR, he recounted, a recent cross‑border “deal sharing” arrangement between his platform and a neighbor depended on quirks in the other platform’s national license that allowed them to invest via a specific vehicle; when they tried to replicate that structure elsewhere, regulators simply said no.

Compliance, in other words, is both bridge and wall: essential for trust and investor protection, but frequently the reason why a promising model works once and then stops.

The UK: from crowdfunding pioneer to private‑markets testbed

If the US is iterating through Congress and SEC guidance, and the EU is rationalizing 27 national regimes, the UK sits in an interesting third position: a mature crowdfunding market now being wired into a broader private‑capital strategy.

Bruce Davis - co‑founder of Abundance Investment and long‑time head of the UK Crowdfunding Association - reminded the audience that the UK’s regulatory framework has always existed on top of its own securities and markets legislation, and that differences at that base layer now translate into divergent crowdfunding models.

On the equity and bond side, platforms are regulated to “arrange deals” and promote them to the public, with explicit responsibilities for segmenting customers and assessing whether an investment is appropriate. Peer‑to‑peer loans sit under a separate regime, where it is the activity rather than the instrument that is regulated, reflecting the fact that P2P emerged before regulation caught up.

Over the last seven years, Davis argued, the UK has shifted away from principles‑based regulation toward product regulation. That shift means supervisors now spend much of their time debating business models with platforms - defining the shape of the product, not just the standards it must meet.

The upside is that crowdfunding is now seen as part of a broader push to “mobilize private capital,” not an oddity on the fringe. New rules for Public Offer Platforms (POPs) and Private Intermittent Securities and Capital Exchange Systems (Pisces) effectively create a continuum:

- Traditional crowdfunding rules apply up to 5 million pounds.

- Above that, POPs enable unlimited offers to the public in the private markets, blurring the line between private and public issuance.

- Pisces provides a framework for intermittent secondary transactions in private company shares - initially conceived as a solution for VC portfolio liquidity, but now opening cautiously to retail.

This architecture makes it easier to imagine a company raising growth capital from the crowd and then offering episodic liquidity events without a full listing, all within one coherent regulatory perimeter.

Secondary markets remain constrained, however. Like their EU counterparts, UK platforms typically operate bulletin boards rather than fully regulated multilateral trading facilities (MTFs). The concern, Davis said, is that importing the full machinery of listed‑market regulation into the crowdfunding context would be prohibitively expensive and inappropriate for smaller tickets.

A more immediate brake on growth is marketing friction. After successive rounds of rule‑tightening, UK platforms now face complex appropriateness assessments and near‑perfect pass‑rate expectations for retail investors, driving up acquisition costs and pushing many players to cut back on marketing. The FCA has launched a discussion paper to review whether those frictions have overshot, opening the door to potential recalibration.

On tokenization, the UK has taken a conservative line: if you tokenize an investment asset, you are still carrying on regulated activity; tokenization does not grant you a different regime. That makes tokenization a technology upgrade rather than a regulatory arbitrage - its value must come from efficiency and better user experience, not lighter rules.

Where the UK really stands out is in tax. The Enterprise Investment Scheme (EIS) and Seed EIS (SEIS) provide generous income‑tax relief on investments into qualifying high‑risk companies (around 30 percent for EIS and 50 percent for SEIS), plus loss relief in certain cases. The Innovative Finance ISA (IFISA) allows investors to hold peer‑to‑peer loans and other qualifying instruments in a tax‑advantaged wrapper, with up to 20,000 pounds in new contributions each year and no tax on income or gains within the envelope.

Davis called these schemes “the one thing we got right” and vowed that the industry would “defend IFISA till we die,” arguing that they have been a key driver of capital into early‑stage and growth companies and a necessary leveler against the attractions of listed markets and pensions.

Karsten Wenzlaff, for his part, sees EIS/SEIS as a model Europe should take seriously - not just as a way to boost crowdfunding volumes, but as a bridge that turns retail investors into tomorrow’s angel investors. The political challenge is that taxation remains a national competence within the EU, and Brussels has historically preferred EU‑wide guarantee schemes over pan‑European tax incentives. That may be shifting as member states hunt for ways to mobilize private capital for energy transition, defense and health, but any UK‑style regime would require both technical and political alignment.

Tokenization, AI and shared infrastructure: tools, not silver bullets

If the first half of the webinar mapped the regulatory terrain, the second half turned to tools: tokenization, AI and shared infrastructure.

Andrew Dix and Sherwood “Woodie” Neiss - author of Investomers and policy expert, were clear that tokenization is no longer hypothetical. US platforms like Republic have already used tokenized securities; firms like Securitize began as enablers and have evolved into marketplaces, and institutions such as Figure have built tokenization stacks from the institutional side. The New York Stock Exchange has announced a tokenized securities exchange, signaling that mainstream market infrastructure is moving in this direction as well.

For Dix, the promise is straightforward: remove intrinsic frictions, reduce costs, improve security, portability and compliance, and enable new categories of assets to reach investors. In today’s analog private markets, humans push paper through fragmented systems. Tokenization and digital market infrastructure could automate large parts of that process, especially when combined with AI.

Yet, as platform builder Konstantin Boyko stressed, technology is the easy part. The harder problems begin when you connect code to real‑world money flows, KYC, payment providers, and multiple jurisdictions. Picking a single payment provider is hard enough in one country; building a stack that gracefully spans regions is far harder.

AI, he argued, could dramatically reduce the burden of drafting and standardizing disclosure documents such as ECSPR’s Key Investment Information Sheet, where lawyers today reinvent the wheel in their own style. That view was echoed across the panel: AI can sit in the background, generating structured, regulator‑aligned templates and freeing human experts to focus on judgment rather than formatting.

Neiss sees an even broader role. The current US disclosure system is “written by lawyers for lawyers,” he said, and is increasingly unusable for the very retail investors it is supposed to protect. AI could help regulators and platforms converge on shorter, more intelligible, yet still compliant disclosures that meet investors where they are and accommodate cross‑border offerings.

On shared infrastructure, Dacxi Chain’s Chief Product Officer Neera Patel sketched a future in which neutral networks and common rails underpin syndicated deals across platforms and borders.

She highlighted three layers:

- Operational efficiency: Issuers launch a deal onto a network and have AI‑infused compliance engines run jurisdiction‑specific checks in parallel, drastically reducing manual legal duplication and accelerating time‑to‑market.

- Investor experience: A shared, verifiable KYC/identity layer -likely based on verifiable credentials - would allow investors to onboard once and then invest across multiple platforms with minimal friction, reducing drop‑off rates and cutting KYC costs.

- Transparency and auditability: Blockchain infrastructure provides an immutable record of allocations, payments, disputes and withdrawals, making it easier for platforms and regulators to monitor the life of a deal - especially when it is syndicated across borders.

Patel was pragmatic about the obstacles. Tax, business‑model economics (e.g., fee split mechanics between platforms), and differing local rules still need human and political negotiation. But those are precisely the topics she believes alliances like GECA should own - creating standards and norms that technology can then codify.

Secondary markets and the search for real liquidity

If there was one theme that united all jurisdictions, it was the sense that primary issuance is only half the story. Without functioning secondary markets, equity crowdfunding will struggle to fulfill its promise.

In the US, the problem is structural. Primary issuance under Reg CF and Reg A is governed at the federal level. Secondary trading, however, falls under state “blue sky” laws, splintering the market into 50 different regimes.

Neiss pointed to the “manual exemption” as one partial workaround: issuers who publish standardized information into a national securities manual - an “Edgar‑lite” - can qualify for exemptions in many states. But the complexity of those rules, and the lack of investor demand for smaller names, have constrained activity. Most meaningful secondary trading in the US still takes place in the Reg D space, on venues like Nasdaq Private Market, Forge and EquityZen, or among larger Reg A+ issuers where investor interest is sufficient to justify the overhead.

Dix did not mince words on the state of US blue sky law: a “Byzantine mess” sustained by state regulators’ desire to preserve their own empires. He argued for a more federalized approach to secondary trading in line with the Clarity Act’s broader effort to update market infrastructure, while acknowledging that current US proposals focus more on digital commodities than tokenized securities.

In the UK, Pisces is an early attempt to square that circle by allowing controlled, episodic liquidity events without the full weight of listing rules. Davis framed the debate in lifecycle terms: different investors want or need to exit at different points, and the system should be able to recycle capital efficiently rather than locking it up until an IPO that may never come.

In Europe, stock exchanges are among the fiercest opponents of any move that might erode their monopoly on secondary trading, and that political reality helps explain ECSPR’s conservative stance on matching engines. But Wenzlaff was blunt: if Europe is serious about financing the green and digital transitions, it will need mechanisms that allow capital from the global north to flow into renewable infrastructure projects in Latin America, Africa and parts of Asia, with credible liquidity options along the way.

Here again, the idea of a shared, decentralized protocol surfaced -not to replace local rules, but to provide a common technical substrate onto which different regulatory wrappers could be mapped.

Why this matters now

The stakes behind this dense, acronym‑heavy conversation are high. For all the technical debate about thresholds, investor tests and SPVs, the through‑line was clear: the world needs more ways for ordinary and professional investors to fund the companies and projects that will shape the next decade - and those channels need to work across borders.

The building blocks are already visible:

- US exemptions that now support meaningful retail participation and are edging toward more inclusive definitions of sophistication.

- A pan‑European license that, once re‑tuned, could allow SMEs to raise up to 12 million euros in a single, cross‑border campaign.

- A UK ecosystem that has quietly invented a tax and regulatory stack for high‑risk private capital, and is now experimenting with POPs and Pisces as bridges into the listed world.

- Tokenization and AI tools that can take friction, cost and opacity out of compliance and operations, rather than adding new layers of hype.

What is missing is coordination - and that, ultimately, is where GECA, EDFA and their partners come in.

As Andy Field closed, the webinar was not intended as an endpoint, but as a starting block. The next step is bringing these conversations into the room: regulators, platforms, academics and technologists meeting face‑to‑face in Malaga this April to move from diagnosis to design.

Dix’s final message was simple and, in its own way, optimistic: the direction of travel is right, even if the pace is frustrating. Progress will depend on exactly the kind of cross‑jurisdictional, cross‑disciplinary dialogue this webinar represented - because in a world where capital, talent and technology are already global, leaving crowdfunding trapped in national silos is no longer a tenable option.

Watch the full webinar here: https://www.youtube.com/watch?v=JhvKrySbAr8

GECA: Frequently Asked Questions

What is GECA?

The Global Equity Crowdfunding Alliance (GECA) is a neutral, industry‑led network that brings together platforms, investors, founders, industry associations, regulators, policymakers and technology providers focused on investment crowdfunding.

Why was GECA created?

GECA was formed because crowdfunding is already global in practice, but fragmented in regulation, infrastructure and coordination, which slows growth and limits cross‑border capital flows.

What problem is GECA trying to solve?

Today, a business that wants to raise capital across borders faces multiple regulatory systems, overlapping compliance regimes and different technology standards, while investors struggle to access opportunities outside their home market.

Is GECA a lobbying organization?

No. GECA’s mission is not to promote one regulatory regime over another but to act as a neutral convening layer that fosters dialogue, alignment and practical pathways for cross‑border collaboration.

Who participates in GECA activities?

Participants include crowdfunding platforms, SME and startup founders, retail and professional investors, national and regional industry bodies, regulators, policymakers and technology providers building market infrastructure.

What is GECA doing in practice, beyond webinars?

GECA is publishing primary‑research‑based white papers, convening working groups with partners like EDFA, and co‑hosting in‑person events such as the April meetings in Malaga to drive regulatory and technical alignment.

How does GECA view emerging tech like tokenization and AI?

GECA sees tokenization and AI as tools to reduce cost and friction in compliance, reporting and cross‑border syndication - not as regulatory shortcuts - and is encouraging shared standards and infrastructure in these areas.

How can I engage with GECA next?

GECA and EDFA are inviting platforms, associations and regulators to the in‑person sessions in Malaga (8–10 April) to continue these conversations through workshops on UX, secondary markets, tokenization and collaboration with academic researchers.

Full Details https://www.crowdfunding-research.org/icafr2026

Register https://www.crowdfunding-research.org/pago

GECA Membership & Participation

Who can join GECA?

GECA welcomes equity crowdfunding platforms, national and regional crowdfunding associations, regulators and policymakers, technology providers, investor associations, researchers and academics.

How do I join GECA?

Visit https://thegeca.org/join to become a GECA member or supporter organization.

What are the benefits of joining GECA?

GECA members gain:

- Access to cross-border dialogue and coordination forums

- Participation in working groups on standards, secondary markets, disclosure templates

- Networking with platforms, regulators, and technology providers globally

- Early access to research, whitepapers, and policy recommendations

- Invitations to GECA events (webinars, workshops, conferences)

- Influence on the development of global crowdfunding infrastructure

Equity Crowdfunding Trends in 2026: From Crowd Capital to Coordinated Capital

(A research-backed trends brief)

Over the past decade, equity crowdfunding has evolved from an experimental financing model into a regulated component of modern capital markets. By 2026, the sector is increasingly characterised not by loosely organised “crowds” but by structured ecosystems combining retail investors, professional capital, and supervised platforms. This transition reflects regulatory consolidation, technological infrastructure development, and the growing integration of crowdfunding into the broader private-capital landscape.

1. From experimental niche to supervised market infrastructure

By 2026, equity crowdfunding (ECF) has moved decisively out of its experimental phase and into the regulated online capital-markets stack. The common pattern across major jurisdictions is the same: clearer operator responsibilities, harmonised rules for cross-border activity, and a sharper distinction between supervised platforms and unregulated campaign websites.

In the European Union, the European Crowdfunding Service Providers Regulation (ECSPR, Regulation (EU) 2020/1503) has created a passport regime under which platforms must be authorised as Crowdfunding Service Providers (CSPs) and may then operate across participating member states under a single rulebook. According to ESMA’s 2024 and 2025 Crowdfunding Market Reports, the EU market now represents low-single-digit billions of euros in annual volume, with a growing share of cross-border activity; equity and equity-like instruments account for a meaningful portion, and retail investors represent the vast majority of participants.[ESMA 2024; ESMA 2025]

In the United States, Regulation Crowdfunding (Reg CF) has stabilised into a predictable retail-access channel: issuers may raise up to 5 million USD in a 12-month period, provided they use a registered funding portal or broker-dealer and comply with Form C disclosure, ongoing reporting, investor-limit, and books-and-records requirements. SEC data and independent industry analyses indicate that, since the 2021 limit increase, median and upper-quartile raise sizes have trended upward, with more campaigns now falling in the 1–5 million USD band—evidence of deal-size maturation rather than a pure micro-raise phenomenon.[SEC Reg CF; KingsCrowd 2025]

In the United Kingdom, post-Brexit reform of the prospectus and public-offer regime has introduced a new Public Offer Platform (POP) framework, with rules taking effect in January 2026. FCA policy statements on the new regime explicitly anticipate that some existing crowdfunding operators will seek POP authorisation, effectively moving parts of the crowdfunding model into a more formal public-offer environment with clearer disclosure and governance expectations.[FCA 2025a; FCA 2025b]

Trend signal: ECF is being pulled into mainstream capital-markets architecture. In the EU, ECSPR consolidates a supervised, passported market; in the US, Reg CF defines a stable exempt-offering lane; in the UK, POP rules invite platforms into a modernised public-offer framework.

2. From “pure crowd” to hybrid: the rise of crowd + professional capital

A key empirical trend is the shift from purely retail-driven campaigns to hybrid capital stacks where professional or sophisticated investors act as anchors, validators, and governance partners.

Large-sample studies of technology-oriented startups and SMEs funded via crowdfunding show that early participation by professional investors -angels, funds, or platform-curated “lead investors” - has a statistically significant positive effect on campaign success, particularly in sectors with high information asymmetry such as IT and deep tech.[Shabbir et al. 2026] Professional involvement functions as a signal of quality and due diligence, reducing perceived uncertainty for retail investors and triggering informed herding behaviour.[Shabbir et al. 2026] Complementary work on sustainable-oriented ventures finds that the human capital of lead investors (experience, reputation, sector expertise) not only raises the probability of funding success but also correlates with better post-campaign performance, especially where projects are complex to evaluate.[Del Sarto et al. 2025]

Across markets, research and platform data indicate that:

- Platforms highlighting co-investment from professional investors or credible institutions see higher conversion rates.

- Campaigns with visible lead investors or platform-endorsed cornerstone commitments attract more and faster retail participation.[Estrin et al. 2022; Moysidou & Hausberg 2020]

Trend signal: In 2026, equity crowdfunding is maturing into coordinated capital: professional anchors plus structured platform screening plus retail participation. For platforms and associations, this elevates the importance of explicit signalling architecture -clear labelling of lead investors, standardised “proof layers” (traction, governance, controls), and transparent screening criteria.

3. Liquidity: from aspirational talking point to design constraint

Illiquidity has long been ECF’s structural weakness. Work on secondary markets in equity crowdfunding highlights how difficult it is to design trading venues for privately issued shares, given challenges around price discovery, information rights, transfer restrictions, and regulatory oversight.[Lukkarinen & Schwienbacher 2024] At the same time, both regulators and industry are experimenting more actively with liquidity mechanisms.

A likely staged pathway - based on current experiments and the secondary-markets literature -may involve:

- Phase 1: Controlled transfers. Limited transfer windows and bilateral transfers via platforms, with issuer consent, basic disclosure updates, and suitability checks.

- Phase 2: Venue partnerships. Selected crowdfunding-issued securities trading on regulated SME growth markets or multilateral trading facilities under specific listing and reporting standards.

- Phase 3: Interoperable rails. Wider interoperability, potentially including tokenised representations to simplify post-trade handling, but still under clear regulatory supervision.

European and national authorities acknowledge that ECSPR itself does not create secondary markets, while noting that the harmonised framework makes such experiments easier to supervise and scale.[ESMA 2024; FMA Austria 2025] Industry commentary similarly treats liquidity not as an optional “nice to have” but as a central design constraint for the next phase of ECF.[Lukkarinen & Schwienbacher 2024; GECA 2025b]

Trend signal: In 2026, the question is less whether liquidity will appear and more how it will be engineered and governed. “Liquidity with integrity” will require minimum issuer-reporting standards, fair-valuation practices, transfer controls, and clear investor-communication norms.

4. Tokenisation: from hype to cautious, infrastructure-first adoption

Tokenisation - representing securities on distributed ledgers with programmable features -has been widely promoted as a solution to private-market frictions. By 2026, the tone has become more cautious and infrastructure-focused.

IOSCO’s Final Report on the Tokenisation of Financial Assets summarises the prevailing regulatory view: tokenisation may improve operational efficiency, settlement, and automation of compliance rules, but it can also introduce or amplify risks, including unclear legal rights, new operational dependencies, and exposure to broader crypto-asset volatility.[IOSCO 2025] The report emphasises technology-neutral regulation: investor-protection and market-integrity standards apply regardless of the underlying ledger, and tokenisation must not obscure what investors actually own or who is accountable.

Surveys of institutional investors and market-infrastructure providers show growing experimentation with tokenised bonds, funds, and equities, but emphasise governance, interoperability, and regulatory clarity as prerequisites for scaled adoption.[EY 2025; Broadridge 2025] For ECF in 2026, the most credible near-term applications appear to be:

- Ledger-based or on-chain cap tables and share registries, tightly linked to legal title.

- Programmable transfer rules encoding regulatory and contractual restrictions into smart contracts.

- Automated compliance and audit trails that simplify reconciliations and supervisory review.[Mubarak & Petraite 2020; IRJMETS 2024; IJNRD 2025]

Trend signal: In 2026, tokenisation’s primary value for ECF is as back-office and compliance infrastructure, not as a retail “crowd token” story. The winning narrative is programmable governance, auditable rights, and supervised trading mechanisms, rather than speculative token trading.

5. AI, analytics, and data standardisation: trust throughput as the new moat

As ECF platforms mature, their competitive edge is shifting from attention capture (marketing reach) to trust throughput: how effectively they can screen deals, detect fraud, match investors, and generate reliable reporting.

ESMA’s most recent crowdfunding market reports explicitly discuss platforms’ current and planned use of AI and machine-learning tools in credit scoring, fraud detection, operational optimisation, and customer support, while flagging governance, bias, and explainability as emerging supervisory concerns.[ESMA 2024; ESMA 2025] In parallel, research on digital trust in platform-based ecosystems shows that digital platform trus t- confidence in the platform’s technological and governance infrastructure - is a critical mediator between firms’ innovation capabilities, crowdfunding outcomes, and technological learning.[Mubarak & Petraite 2020; Shabbir et al. 2026]

Shabbir and co-authors propose and test a capability-trust-crowdfunding pathway in which:

- Firms’ dynamic capabilities, digitalisation, and networking capabilities increase digital trust in crowdfunding platforms.

- Digital platform trust then boosts crowdfunding performance.

- Crowdfunding, in turn, enhances technological learning and innovation.[Shabbir et al. 2026]

They also emphasise that digital trust increasingly rests on transparency, immutability, and verifiability, with blockchain and advanced analytics playing a central role.[Mubarak & Petraite 2020; Shabbir et al. 2026]

Trend signal: In 2026, leading platforms increasingly:

- Enforce structured issuer disclosures and machine-readable data templates.

- Use AI/analytics for pre-screening, anomaly detection, and monitoring- with human oversight and documented model governance.

- Provide standardised KPI dashboards and reporting cadences to investors and regulators.

- Treat digital trust architecture as a first-order design problem, not an afterthought.

For regulators, AI and structured data are moving into the core of the supervisory conversation. For infrastructure providers and associations, this validates the need for shared data schemas and evidence layers that make platforms more comparable and exam-ready.

6. Cross-border ambition meets compliance realities

For more than a decade, “cross-border crowdfunding” was mainly an aspiration. By 2026, it is practically achievable in specific regions -but success depends on standards rather than slogans.

In the EU, ECSPR’s passport mechanism allows an authorised CSP in one member state to provide services across all participating states under a single authorisation, subject to notification procedures.[EC 2020; ESMA 2024] ESMA’s data and Eurocrowd’s commentary show that a growing share of campaigns now attract cross-border investors or involve cross-border issuers, and some platforms explicitly position themselves as pan-European marketplaces.[ESMA 2025; Eurocrowd 2026; Eurocrowd 2025] National regulators, such as the Austrian FMA, broadly welcome the creation of a genuinely European market but highlight challenges around language, disclosure comparability, marketing rules, and cross-border enforcement.[FMA Austria 2025]

Research on crowdfunding in emerging markets points to similar dynamics. Tajul Urus and co-authors note that as more emerging economies adopt crowdfunding frameworks, differences in regulatory maturity, enforcement, and governance create both opportunities and risks.[Tajul Urus et al. 2025] They emphasise that platform-level governance, disclosure quality, and accountability mechanisms are critical to building trust in markets where formal rules and supervisory capacity are still evolving.

Trend signal: In 2026, cross-border ECF is primarily constrained by:

- Disclosure and data interoperability (so investors and supervisors can understand and compare offers).

- Investor categorisation and suitability frameworks (to avoid regulatory arbitrage and mis-selling).

- Books-and-records standards (so authorities can rely on each other’s platforms’ evidence).

This is where neutral trust and evidence layers - systems that capture platform activity, disclosures, risk acknowledgements, orders, and funds flows in a tamper-evident, portable form - add structural value. They make it easier for platforms to rely on each other’s gatekeeping, for regulators to examine cross-border activity, and for investors to trust that foreign campaigns sit on robust compliance rails.

7. ESG, verticalisation, and the need for evidence-rich disclosures

Equity crowdfunding is also undergoing vertical specialisation: climate and clean energy, real estate, local infrastructure, and impact ventures are emerging as distinct segments with their own norms and expectations.

An fsQCA study of 88 solar crowdfunding projects in Spain and Italy finds that low perceived risk and short maturity periods are more consistently associated with funding success than high environmental impact alone; CO₂-saving metrics enhance appeal but are not sufficient by themselves.[Santos-Rojo et al. 2025] The authors conclude that retail “green” investors behave as conservative capital: they care about environmental outcomes but retain strong preferences for capital preservation and liquidity. Other work on sustainable-oriented ventures funded via ECF shows that lead investors’ expertise and credibility matter especially in ESG contexts, because projects are complex to evaluate and impact is hard to verify.[Del Sarto et al. 2025]

Trend signal: In 2026, vertical segments such as climate/energy and real estate increasingly require:

- Domain-specific disclosure templates (e.g., project economics, technical risk registers, impact metrics, verification sources).

- Clear risk-grading and maturity profiles expressed in plain language.

- Third-party validation or assurance of key technical and impact metrics.

- Evidence layers that surface the underlying assumptions, monitoring history, and governance practices, beyond marketing narratives.

Platforms that treat ESG offerings as “just another pitch” risk mis-pricing and mis-selling; those that build structured, evidence-rich disclosures and monitoring will be better positioned with both investors and regulators.

8. Macro sensitivity, consolidation, and sustainability of the model

Synthesised work on crowdfunding and macroeconomic dynamics suggests that ECF is macroeconomically sensitive rather than counter-cyclical by default. Summarising prior empirical and theoretical work, Wille argues that crowdfunding volumes respond to variables such as unemployment, interest rates, and policy uncertainty, and that in some contexts crowdfunding can act as a partial substitute for bank lending and venture capital when traditional credit tightens.[Wille 2025] At the same time, different forms of uncertainty have different effects: some measures of economic policy uncertainty can increase small-ticket, local-project participation, while heightened geopolitical risk often suppresses risk appetite.

On the micro side, supervisory reports and industry commentary point to platform consolidation and sustainability pressures. Authorisation costs, ongoing compliance obligations, competition for high-quality deal flow, and plateauing conversion rates in some saturated markets are driving weaker or under-capitalised operators out, while better-governed platforms gain share.[ESMA 2025; GECA 2025a; GECA 2025b] Post-campaign data -defaults, follow-on funding, dilution, and exits -also highlight that, like other early-stage asset classes, equity-crowdfunded portfolios are highly dispersed, with a minority of campaigns generating outsized returns and many underperforming.[Lukkarinen & Schwienbacher 2024; Tajul Urus et al. 2025; Santos-Rojo et al. 2025]

Trend signal: In 2026, policymakers increasingly see ECF as part of macro-sensitive alternative finance and focus on:

- Harmonised regimes (ECSPR, POP, Reg CF) that manage risk coherently.

- Platform-level resilience, governance, and data-quality expectations.

- Greater transparency around post-campaign performance to avoid unrealistic retail expectations.

For platforms, the implication is that long-term viability will depend less on raw campaign volumes and more on governance quality, trust architecture, and evidence-backed performance.

9. The 2026 inflection: from crowd-powered to coordinated capital

Bringing these threads together, 2026 looks like an inflection point where equity crowdfunding transitions from crowd-powered to coordinated capital:

- Regulated rails expand and harmonise (ECSPR in the EU, POP in the UK, Reg CF in the US), pulling ECF into mainstream capital-markets infrastructure.

- Hybrid capital stacks become normal, with professional anchors and platform screening shaping retail flows and post-campaign outcomes.

- Liquidity and tokenisation move from aspirational talking points to cautiously engineered mechanisms centred on governance, rights clarity, and investor protection.

- AI and structured data become core to both platform differentiation and supervisory scrutiny, with digital platform trust mediating innovation outcomes.

- Cross-border activity is enabled by passports but fundamentally constrained by disclosure comparability, investor categorisation, and books-and-records standards.

- Vertically specialised segments, especially in ESG, demand evidence-rich, verifiable disclosures and domain-specific governance.

In that environment, decisive advantages shift away from marketing and toward trust architecture:

- Shared data schemas and disclosure standards.

- Verifiable, tamper-evident evidence of platform and issuer behaviour.

- Robust digital-trust mechanisms that allow regulators, investors, and partner platforms to rely on what the rails say happened.

Equity crowdfunding is no longer just a way to mobilise the crowd; it is becoming one of the coordinated mechanisms through which private capital is raised, governed, and - eventually - traded.

References

Broadridge. 2025. Next-Gen Markets: The Rise and Reality of Tokenization. Broadridge Financial Solutions Industry Report.

Del Sarto, N., Di Pietro, F., and B. Prencipe. 2025. “Equity Crowdfunding for Sustainable-Oriented Ventures: The Role of Lead Investors’ Human Capital.” Journal of Business Venturing Insights.

ESMA (European Securities and Markets Authority). 2024. Market Report: Crowdfunding in the EU 2024.

ESMA (European Securities and Markets Authority). 2025. Market Report: Crowdfunding in the EU 2025.

Eurocrowd. 2025. “French and Italian Crowdfunding Trends: A Comparative ECSPR Monitor.” European Crowdfunding Network Report.

Eurocrowd. 2026. “ESMA Crowdfunding Market Data 2024.” Eurocrowd Market Commentary.

- 2025. Institutional Investor Digital Assets Survey. Ernst & Young Global Financial Services Report.

FCA (UK Financial Conduct Authority). 2025a. PS25/9 – New Rules for the Public Offers and Admissions to Trading Regime (Public Offer Platforms).

FCA (UK Financial Conduct Authority). 2025b. PS25/10 – Final Rules for Public Offer Platforms.

FMA Austria. 2025. “ESMA Report on the European Crowdfunding Market – National Commentary.” Austrian Financial Market Authority Briefing.

GECA (Global Equity Crowdfunding Alliance). 2025a. Eight Pivotal Trends Reshaping Equity Crowdfunding in 2025.

GECA (Global Equity Crowdfunding Alliance). 2025b. The $1 Trillion Liquidity Opportunity in Equity Crowdfunding.

IOSCO (International Organization of Securities Commissions). 2025. Tokenisation of Financial Assets: Final Report.

IRJMETS. 2024. “Crowdfunding Using Blockchain – Trust and Fraud Prevention.” International Research Journal of Modernization in Engineering Technology and Science.

IJNRD. 2025. “Trust and Fraud Prevention: A Blockchain-Based Crowdfunding Framework.” International Journal of Novel Research and Development.

KingsCrowd. 2025. Investment Crowdfunding Annual Report.

Lukkarinen, A., and A. Schwienbacher. 2024. “Secondary Markets in Equity Crowdfunding.” In Palgrave Encyclopedia of Private Equity.

Moysidou, K., and J. P. Hausberg. 2020. “In Crowdfunding We Trust: A Trust-Building Model in Crowdfunding.” Journal of Business Venturing Insights.

Mubarak, M. F., and M. Petraite. 2020. “Digital Trust in Industry 4.0 Ecosystems: The Role of Blockchain and Advanced Analytics.” Technological Forecasting and Social Change.

Santos-Rojo, C., J. Gallego-Nicholls, and A. Rey-Martí. 2025. “Understanding Investor Behavior in Crowdfunding for Sustainability: An fsQCA Study.” Environment, Development and Sustainability.

SEC (U.S. Securities and Exchange Commission). 2017 (updated). Regulation Crowdfunding: Small Entity Compliance Guide for Intermediaries.

Shabbir, M., Petraite, M., Mubarak, M. F., Gobakhloo, M., and A. Rasli. 2026. “More than Money: Strategic and Operational Innovation Capabilities to Promote Technological Innovation through Crowdfunding.” Financial Innovation 12(21).

Tajul Urus, S., I. S. Mohamed, Z. Abd Rasit, and M. Mohamad. 2025. “Crowdfunding in the Emerging Market: Insight into the Conceptualization and Governing Issues of Crowdfunding.” International Journal of Research and Innovation in Social Science 9(4): 562–571.

Wille, N. 2025. “Crowdfunding and Macroeconomic Dynamics.” SSRN Working Paper Series.

GECA - Frequently Asked Questions

Q1. What is GECA?

The Global Equity Crowdfunding Alliance (GECA) is a non-profit industry alliance that brings together equity crowdfunding platforms, national associations, regulators, and technology partners to make equity crowdfunding more borderless, interoperable, and trusted worldwide.

Q2. Why does GECA matter if we already have ECSPR, Reg CF, and the UK POP regime?

Regimes such as ECSPR in the EU, Regulation Crowdfunding in the United States, and the UK’s Public Offer Platform (POP) framework define how crowdfunding operates within their respective jurisdictions.

However, these regimes do not by themselves solve fragmentation between jurisdictions, platforms, and data standards.

GECA focuses on the gaps at the edges by:

- Improving cross-border understanding between platforms and regulators

- Encouraging compatible standards across jurisdictions

- Supporting platforms that operate in multiple markets

Q3. What are GECA’s main objectives?

Based on its public statements and activities, GECA focuses on five main objectives:

- Advocacy and education - explaining the role of equity crowdfunding in modern capital markets and helping address common misconceptions.

- Policy dialogue and harmonisation - acting as a structured counterpart for regulators and policymakers working on crowdfunding, secondary markets, and related regulation.

- Ecosystem building - connecting platforms, service providers, and associations that would otherwise operate in isolation.

- Research and insight - surfacing global trends, risks, and opportunities to inform better regulation and business strategy.

- Standards and best practices - encouraging common approaches to disclosures, risk labelling, operational resilience, and cross-border practices.

Q4. How does GECA relate to the 2026 “coordinated capital” trend?

The article describes equity crowdfunding in 2026 as moving from “crowd-powered” to “coordinated capital” - where regulated rails, professional investors, and trust infrastructure increasingly shape market outcomes.

GECA’s role is to support that shift at a global level by:

- Providing a forum where platforms and associations can align on disclosure, governance, and investor-protection expectations

- Helping regulators identify where fragmentation or unintended frictions are limiting coordinated capital formation

- Highlighting successful models for hybrid investment rounds, liquidity mechanisms, and cross-border collaboration

Q5. Who can be involved in GECA?

GECA aims to support a broad membership base that may include:

- Equity crowdfunding platforms and investment platforms

- National and regional crowdfunding or fintech associations

- Professional investors and ecosystem partners such as law firms, auditors, and data providers

- Regulators and policymakers participating as observers or dialogue partners

The aim is not to create a closed club, but a representative forum for the global equity crowdfunding ecosystem.

Q6. What practical value does GECA offer to platforms?

For platforms, GECA can provide:

- Early visibility into regulatory and market trends affecting cross-border operations, secondary markets, and institutional participation

- Access to peers addressing similar challenges, such as liquidity design, disclosure standards, AI use in due diligence, and tokenisation infrastructure

- Opportunities to help shape common templates and guidelines that may later be referenced by regulators or investors

- Increased international visibility through joint research, events, and ecosystem communications

Q7. How does GECA support regulators and policymakers?

Regulators and policymakers can use GECA as a channel to:

- Understand how rules are functioning in practice across different markets

- Hear from a diverse set of platforms and associations rather than only the largest or most visible actors

- Explore the implications of emerging tools such as AI in due diligence, tokenised securities, and secondary market infrastructure in a structured dialogue

This can help inform future adjustments to ECSPR, Reg CF, the UK POP regime, and other national frameworks in a more evidence-based and internationally informed way.

Q8. How does GECA fit into the future of equity crowdfunding?

As equity crowdfunding becomes more regulated, more hybrid, and more interconnected, coordination outside formal regulation becomes increasingly important.

GECA’s role is to:

- Support alignment rather than fragmentation in disclosures, governance practices, and market expectations

- Showcase successful models from different regions and industry verticals

- Help the ecosystem move from one-off national experiments toward a more coherent global architecture for equity crowdfunding

In that sense, GECA is one of the actors helping the sector complete the transition described in the article - from isolated “crowd capital” experiments toward a coordinated and trusted layer of the private-capital market.

These Trends Don't Build Themselves

The coordinated capital era requires coordinated action - across borders, platforms, and stakeholders. GECA is where that coordination happens.

Join us in building:

✅ Cross-border disclosure standards

✅ Liquidity infrastructure

✅ Trust architecture that scales globally

👉 Join GECA today and shape the future of equity crowdfunding.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Diaspora Capital & Ethiopian Crowdfunding: Meseret Warner's Vision | GECA Podcast

Diaspora Capital & Ethiopian Crowdfunding: Meseret Warner's Vision | GECA Podcast

Most diaspora send money home as gifts. What if those billions became investments instead?

Over $100 billion flows into Africa annually as remittances – consumed, gifted, never invested. Meanwhile, 95% of Ethiopian businesses can’t access traditional finance due to lack of collateral. What if redirecting even a fraction of diaspora capital could change entire economies?

Join Andy Field in conversation with Meseret Warner, founder of Ignite Investment (Ethiopia’s first equity crowdfunding platform) and GECA Steering Committee member, as she reveals how to bridge the gap between diaspora capital and African entrepreneurship. From IT developer in Canada to pioneering fintech in Ethiopia, Meseret shares the trust-building journey required to convert remittance senders into equity investors.

From proving the concept through digital marketing alone (raising millions before building a platform) to navigating Ethiopia’s regulatory sandbox, Meseret breaks down why trust matters more than technology, how to make companies “crowdfund ready,” and why women entrepreneurs actually repay debt at higher rates than men.

Key insights:

- Why diaspora communities are emotionally invested – not just financially

- How to convert one-way remittance flows into two-way equity investments

- The critical role of regulatory sandboxes in emerging markets

- Why 65% of Ignite’s funded companies are women-led enterprises

- How partnerships with GIZ and African Development Bank enable scaling

- The coordination gap: why retail investors face barriers high net worth individuals don’t

- What incremental progress in the UK, US, and Ethiopia signals for global crowdfunding

Remittances fund consumption. Investment builds economies.

ALSO AVAILABLE ON

![]()